Asia Pacific is home to many of the world’s premier ski destinations, with Japan a major highlight as winter descends from as early as November. With the Covid-19 pandemic fading from memory, skiers and travellers alike are returning to Japan’s snowy slopes more than ever, in another sign of the robust travel recovery in Asia Pacific.

In fact, Visa cardholder data analysed by Visa Destination Insights reveals not only is Japan now the ski destination of choice in the winter season, but skiers do more than slalom at the ski resorts. In fact, ski travel is a catalyst for tourism across Japan as skiers venture to other parts of the country as part of their “après-ski” or post-skiing activities.

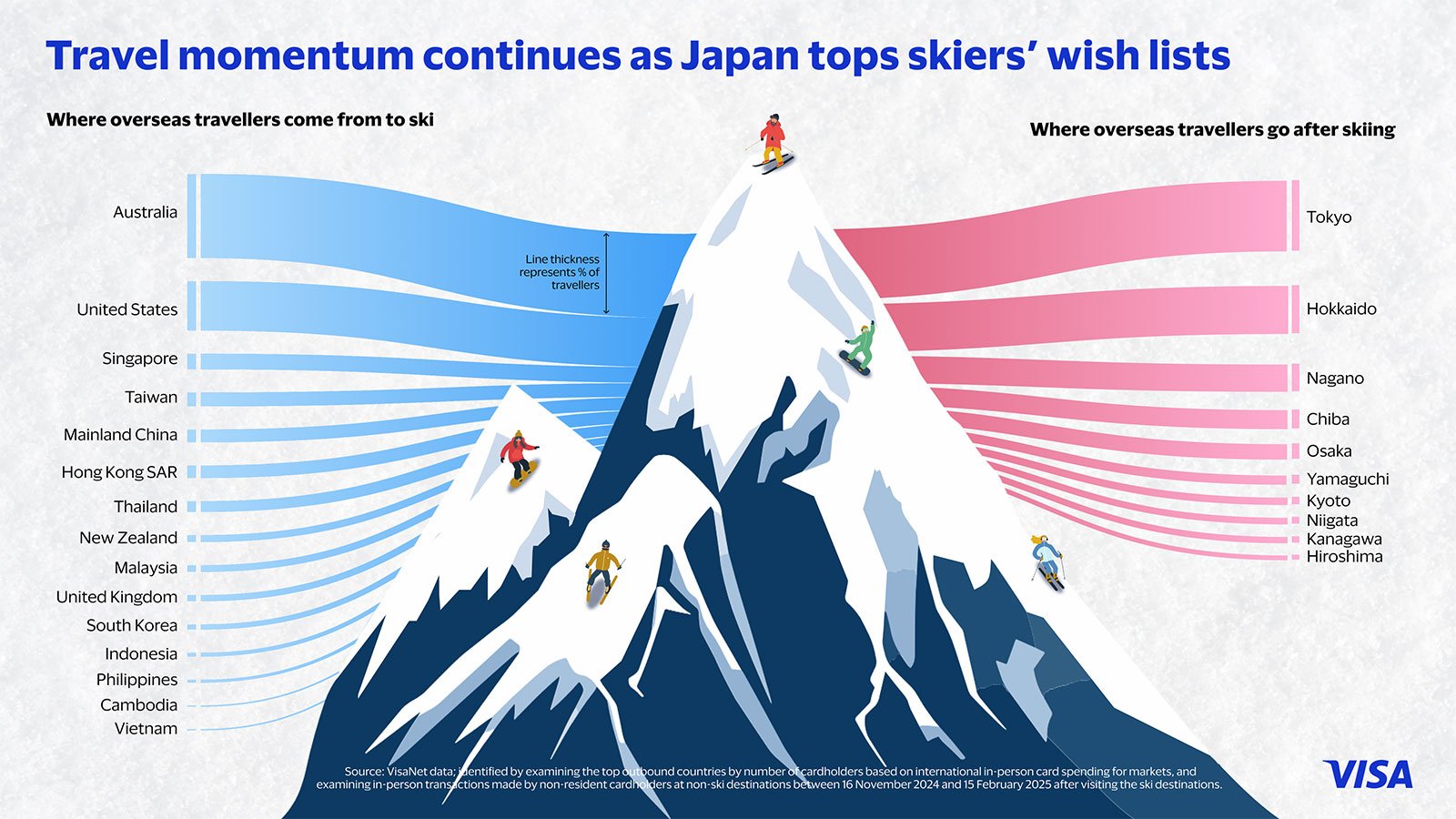

Travel momentum continues as Japan tops skiers’ wish lists

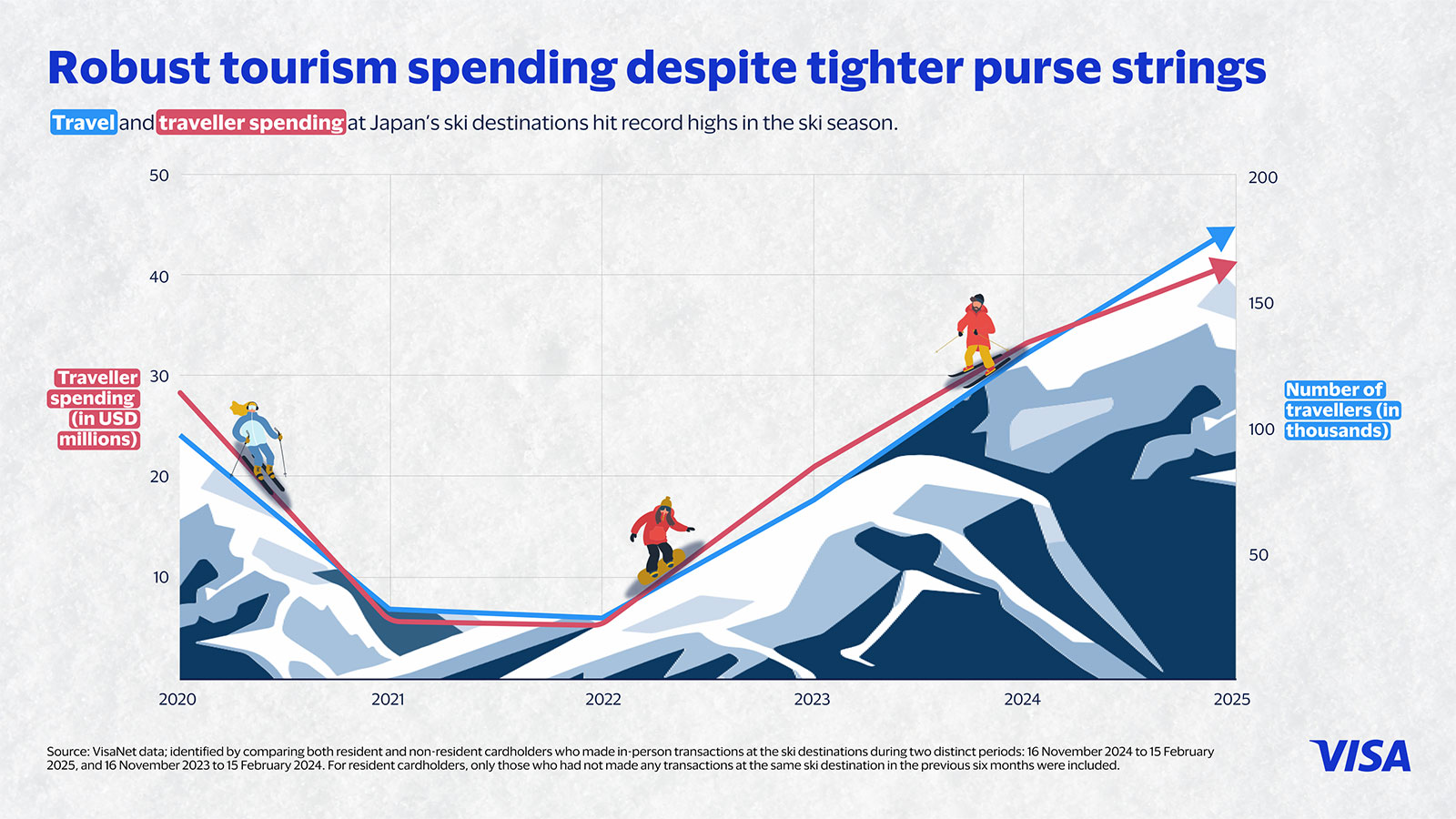

Ski travel is not just returning to Japan – it is setting new records. According to Visa data, the number of visitors into Japan’s ski destinations¹ during the peak of the ski season from November 2024 to February 2025 grew approximately 40 percent year-on-year². This is after ski travel already exceeded pre-pandemic levels during the same period from 2023 to 2024.

Importantly, Japan is emerging as the ski destination of choice in the ski season, especially for Asia Pacific travellers. In fact, it is the number one destination for Asia Pacific travellers as a whole and newly number one for Mainland China visitors, dethroning the United States which topped the list last year. For Australian travellers, Japan is ranked second just behind New Zealand³.

Based on Visa data, overseas travellers to Japan’s ski destinations accounted for about 80 percent of all travellers while domestic travellers accounted for around 20 percent⁴. The growing global allure of Japan’s ski destinations is also reflected in the approximately 50 percent growth in overseas travellers' year-on-year, compared to around 20 percent growth in domestic travellers⁵.

Australians top the list, representing about 30 percent of all overseas travellers to Japan’s ski destinations, while United States is second at about 20 percent. Southeast Asians especially from Singapore, Thailand, and Malaysia account for approximately 15 percent of all overseas travellers, while Mainland China represents around 5 percent.

Cautious consumer spending fails to dampen tourism impact

The record levels of ski travel into Japan are translating into robust travel spending, even as travellers tighten their purse strings. Visa data showed an approximate 40 percent year-on-year surge in cardholder transactions at Japanese ski destinations during the ski season, while total spending grew by around 25% year-on-year.

Overseas travellers contributed the lion’s share of spending at ski destinations at about 90%. Year-on-year, the total volume of overseas travel spending at the destinations also grew about 30%, mirroring the growing allure of Japan’s ski resorts worldwide.

While Entertainment, Lodging, and Restaurants accounted for about 50 to 70 percent of spending by both overseas and local travellers, overseas travellers spend a much larger proportion of their budgets on entertainment (~40%), such as onsens (hot springs), childcare, and local tours unique to each ski resort.

What this means: Ski resorts should do more than just promoting their skiing facilities to potential travellers, who seek a complete experience onsite. While skiing is the main draw, resorts that showcase the full range of experiences that travellers can enjoy at their resorts, either through their own promotions or with online travel agencies and airlines, may well capture more growth.

With consumers cautious with spending, ski resorts may also consider offering curated packages that give travellers access to a full range of amenities, delivering more bang for their buck.

A “Big Three” is emerging among ski resorts, but crowds differ

Japan is home to several destinations but three are proving to be the most popular – Niseko, Hakuba, and Furano. Not only do they account for the majority of cardholder spend according to Visa data, but they also have the fastest rate of traveller growth year-on-year at about 35, 45, and 50 percent, respectively.

Niseko and Hakuba have been a hotspot for overseas skiers in recent years. In fact, Niseko accounts for nearly half of overseas visits and more than half of spending from November 2024 to February 2025. Hakuba, often called the “Second Niseko” and boasting easy access from Tokyo is second, accounting for approximately 35% of overseas visits and is the fastest growing by overseas card spend year-on-year.

On the other hand, Furano is a local favourite, accounting for more than half of all domestic visits. But overseas skiers are fast adding it to their plans as they seek to explore all of Japan’s slopes, with Furano the fastest growing resort by overseas visits at around 70 percent year-on-year.

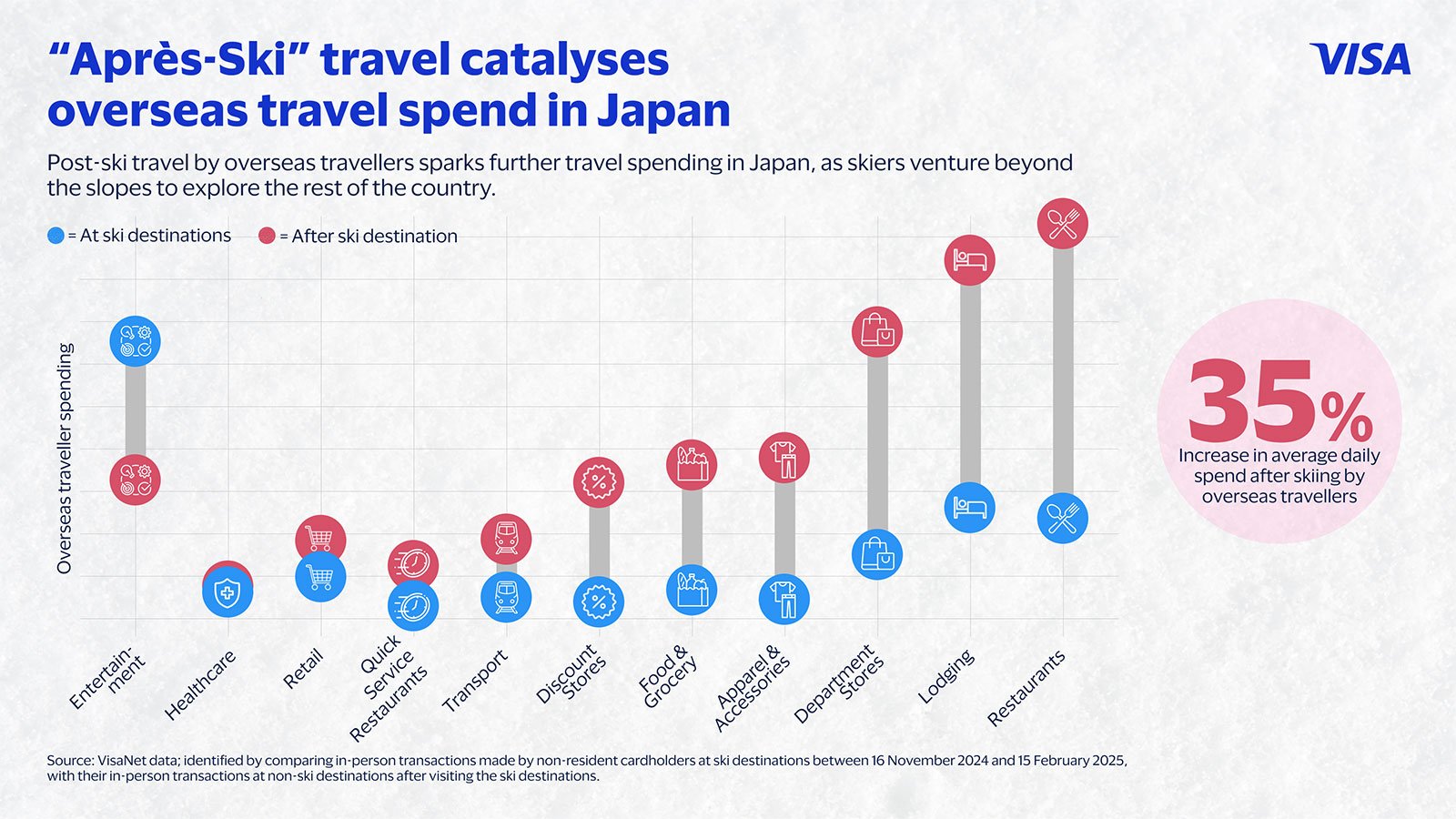

“Après-ski” travel catalyses overseas travel spend in Japan

Among skiers, “après-ski” refers to activities that skiers engage in after a day of skiing, from cosy gatherings to parties that bring the community together. Visa’s analysis found that just like how skiers enjoy their post-skiing hours, they also plan additional travel to explore the rest of Japan after their stays at ski resorts.

According to Visa data, more than 90 percent of international ski travellers at ski destinations venture to other regions in Japan after they ski, spending nine more days on average. They also spend more than at their ski destinations at about 35 percent more per day⁶.

What this means: Merchants in Chiba, Tokyo, and Osaka should be on alert as they receive the highest influx of post-ski travellers beyond the ski regions, although a significant proportion of travellers venture to nearby Hokkaido and Nagano after they ski⁷. They are on a retail and dining streak to experience Japanese culture and products, with over half of spending on restaurants, department stores, clothes, and even luxury shopping.

Merchants, particularly those in these hotspots, can tailor products and promotions to this group of post-ski travellers. Examples include targeted dining and retail deals for consumers who are visiting after staying at ski resorts and for merchants in Hokkaido and Nagano, or targeted partnerships with ski resorts to offer affiliated deals for those coming down from the ski slopes.

Card issuers can capture this growth by deepening merchant partnerships in these hotspots, with curated shopping guides and targeted promotions that ease travel and shopping experiences.

Visa Consulting and Analytics (VCA) harnesses Visa’s payments expertise and proprietary analytics to deliver insights that drive better business outcomes and improve customer journeys. We help clients formulate strategies to capture the biggest payment opportunities, optimise portfolios, and execute on digital more effectively. Learn how you can work with VCA here.

_________________________________________________

¹ For simplicity in this analysis, ski destinations are defined by the specific city, town, village, or ward where popular ski resorts are located, using the most granular level available. The regions covered include: Niseko, Kutchan, Rankoshi, Yamanouchi, Yamagata, Furano, Nozawaonsen, Hakuba, and Yuzawa.

2 Identified by comparing both resident and non-resident cardholders who made in-person transactions at the ski destinations during two distinct periods: 16 November 2024 to 15 February 2025, and 16 November 2023 to 15 February 2024. For resident cardholders, only those who had not made any transactions at the same ski destination in the previous six months were included.

³ Identified by examining the top outbound countries by number of cardholders based on international in-person card spending for countries in the Asia Pacific region between 16 November 2024 to 15 February 2025.

⁴ Identified by comparing both resident and non-resident cardholders who made in-person transactions at the ski destinations during two distinct periods: 16 November 2024 to 15 February 2025, and 16 November 2023 to 15 February 2024. For resident cardholders, only those who had not made any transactions at the same ski destination in the previous six months were included.

⁵ Identified by comparing both resident and non-resident cardholders who made in-person transactions at the ski destinations during two distinct periods: 16 November 2024 to 15 February 2025, and 16 November 2023 to 15 February 2024. For resident cardholders, only those who had not made any transactions at the same ski destination in the previous six months were included.

⁶ Identified by comparing in-person transactions made by non-resident cardholders at ski destinations between 16 November 2024 and 15 February 2025, with their in-person transactions at non-ski destinations after visiting the ski destinations.

⁷ Identified by examining in-person transactions made by non-resident cardholders at non-ski destinations between 16 November 2024 and 15 February 2025 after visiting the ski destinations.